{kind=link}

This is a prior version of the COVID-19 Economic Crisis: by State Report. Please find the most recent version here.

Infographic: July 2021 COVID-19 Jobs Report Data

Key Findings

All but two states still have fewer jobs overall than they did in February 2020, but many industries in many states are returning to pre-recession levels.

For the first time since the beginning of the recession, fewer than 20 states are down in jobs more than 5%—16 in total.

In almost every state, low-wage industries are down the most jobs.

Net job loss since February 2020 in hotels and restaurants range hugely from highs of 41% fewer jobs in Washington, DC and 27.2% fewer jobs in New York to a jobs gain in Idaho of 1.7% and losses of less than 2% in Montana and Oklahoma and 6% in Texas—through July.

With the strongest national job growth yet in 2021 and 38 states seeing statistically significant employment increases, July continued recent encouraging trends for the country’s economic trajectory. Even with well over four million jobs gained so far in 2021, however, all but two states are still short of their February 2020 employment levels. Nationally, payroll employment is still down 5.7 million jobs—a 3.7 percent shortfall—from February 2020, highlighting how far the economy sank last year.

The country’s pace of progress moving forward will depend on vigilance and responsiveness to changing circumstances as the country and world find their way after unique, intertwined, public health and economic shocks.

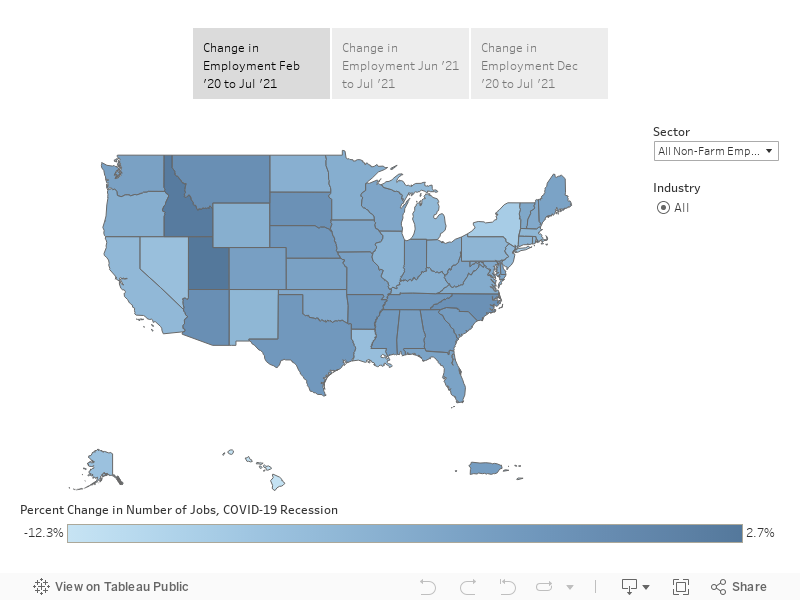

Map 1 compares states in the percent change in the number of payroll jobs for several time periods. The selectors at the top of the map allow users to toggle between the change in employment between February 2020 and July 2021, the change for 2021 through July, and the change in employment for only the last month: June to July. Selecting a state on the map will reveal the change in the number of jobs over the period as well as the percent change. The data are from Bureau of Labor Statistics’ (BLS) monthly surveys from the February 2020 to July 2021 surveys (covering payroll periods containing 12th day of each month).

Map 1: Change in Employment, June 2021 to July 2021

- Employment data used here are seasonally adjusted, meaning that the Bureau of Labor Statistics accounts for normal seasonal variation in employment due to various factors.

- Small differences between states in the percent job change may not be statistically significant.

As of July 2021 the largest net state job shortfall since February 2020 was in Hawaii, which is down 12.0% of its pre-pandemic employment. Hawaii is followed by New York, Alaska, Nevada, and Louisiana, which are down 9.0%, 7.6%, 7.4%, and 7.2% respectively. Two states, Utah and Idaho, have seen job increases from February 2020 to July 2021, with gains of 2.7% and 2.2% respectively. These states had been among the fastest growing prior to the pandemic, ranking sixth and second respectively in February 2019 to February 2020 job growth.

Sixteen states are still down more than 5% of their jobs relative to before the pandemic. The industries that were hit hardest continue to be down substantial numbers of jobs in most states. Many industries are, however, starting to return to pre-COVID levels of employment in a number of states.

The hardest hit sector continues to be Leisure and Hospitality, in which, nationally, the Accommodation and Food Services industry is still down 9.3% of its employment (1.3 million jobs) and the Arts, Entertainment, and Recreation industry 16.1% (403,000 jobs). July marked the first month since the recession started in which Accommodation and Food Service jobs were down less than 10% from February 2020. New York is, however, still down 27.2% of its jobs in this category, the worst in the nation, with Alaska and Hawaii following with job shortfalls of 24.6% and 24.4% respectively.

State and local government employment has notably fallen across the country. In the United States overall, state government employment is down 4.3% from February 2020 to July 2021 and local government employment has been reduced by 3.9%. State and local governments combined are down over 800,00 jobs. From February 2020 to July 2021, Ohio has reduced its state employment by 10.8%, the largest decline in the country, with North Carolina dropping the next most at 9.5%. Local government employment is down the most in Kentucky, at 12%. It is followed by New Jersey at 9.2% and New Mexico at 8.0%.

As discussed more later, the labor-intensive Health Care and Social Assistance industry has contributed greatly to total job losses in most states, with payroll employment down 747,000 nationally—though in percentage terms it has been less hard hit than the hardest-hit industries, having lost 3.6% of jobs nationally as of July.

Professional, Scientific and Technical Services, and Finance and Insurance, are the only two private industries that have returned to their pre-COVID level of employment nationally and have fully recovered in 31 and 21 states respectively. Other industries have recovered to pre-COVID levels of employment in a number of states—Construction has returned to pre-recession levels in 12 states, Manufacturing in 8, and Retail Trade has recovered in 11 states, for example.

Overall, progress back to pre-recession levels in 2021 has varied significantly among states. Hawaii, Vermont, Minnesota, Rhode Island, and Nevada have seen the strongest job growth so far this year relative to their February 2020 employment levels. The slowest growing states by this measure have been Wyoming, Alaska, Virginia, Louisiana, and Alabama. For all of these states except Nevada and Rhode Island, their ranking is closely correlated with their Accommodations and Food Service Industry employment. Although the overall jobs picture is driven by multiple industries in all of these states, in the case of Nevada and Rhode Island growth in the Accommodations and Food Service Industry has been typical while other industries have been particularly strong. Rhode Island and Nevada rank particularly high in job growth in Manufacturing. Nevada leads the country in Retail job Growth and is second in Professional and Business Services sector job growth. Rhode Island is first in Health Care and Social Assistance and Construction job increases for the year.

Map 1 can display individual sectors and industries as well as employment for all sectors and industries. Descriptions of each sector and industry can be found on the BLS website. The table in addendum 1 shows a top-to-bottom ranking, sortable by state name or employment change from February 2020 to the latest month, for 2021 only, or for the most recent month. The table can list employment for all sectors and industries, or individual sectors and industries.

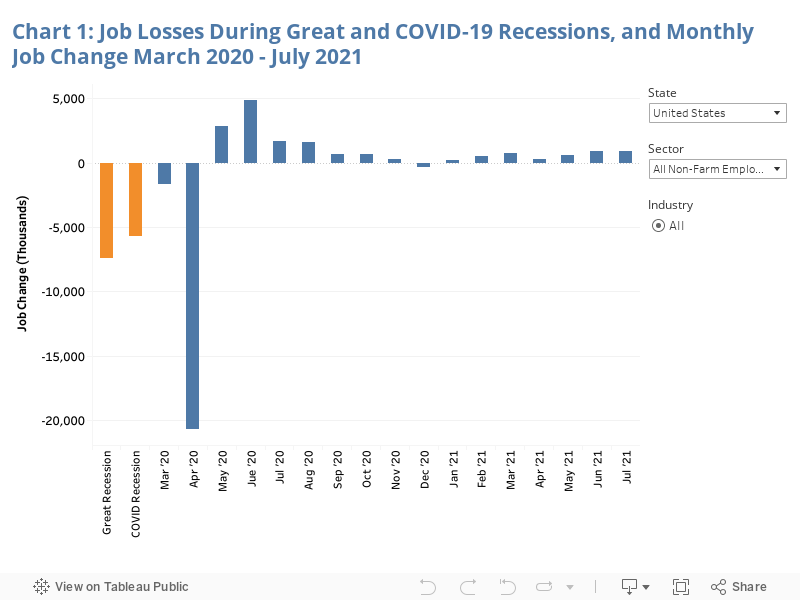

Chart 1 compares (1) the change in number of jobs during the Great Recession (December 2007 to June 2009), (2) job loss in the current crisis from February 2020 and (3) job change in each month from March 2020 through the latest month. Comparisons can be viewed for the nation or a selected state, district, or territory as well as for total payroll employment or a selected sector or industry.

- Employment data are seasonally adjusted.

The overall picture is one of an economic recovery that had fallen off over the second half of 2020 and into January 2021, with a pickup starting in February. In total employment as of June, 20 states were down more jobs than they lost from their peak employment to their low point in the Great Recession. Forty-five states are still down more jobs than during the Great Recession in Accommodation and Food Services, 31 are down more in Heath Care and Social Assistance, 30 in local government, and 24 are down more in state government.

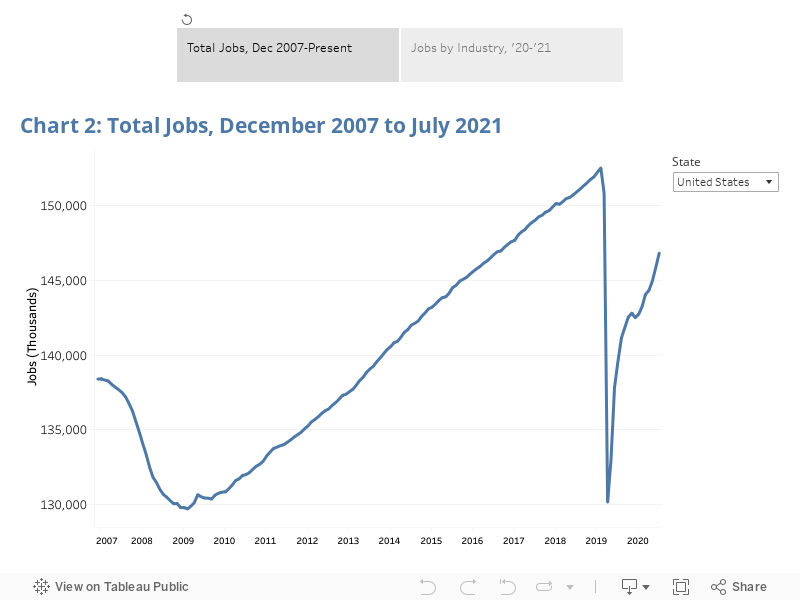

Chart 2 shows in stark fashion the extent of job loss at the beginning of the pandemic, the immediate partial bounce back, the slowing of the recovery, and the turnaround in February. Between February and April 2020, in almost every state, all or most of the jobs gained since the Great Recession were lost. This marked a sharp reversal from the steady climb seen nationally that began in 2010, accelerated starting in 2012, and had slackened in the last few years. The sharp drops of March and April 2020 reversed in May of the year, but the rate of progress slowed and even reversed in some states at the end of 2020 and into January 2021. Starting in February of this year, growth again accelerated.

- Employment data are seasonally adjusted.

The path of the economy has been influenced by the prevalence of COVID-19 and the federal government’s response. The first flood of cases in early 2020 caused massive job losses. The economy began to bounce back as governments responded, cases declined, and businesses and people adjusted. In the latter half of 2020 and into January 2021, however, cases again rose and federal government support tailed off, leading to a slowing of economic progress. As strong steps by the federal government started to have an impact in February and March and optimism about the health situation grew, the economy regained positive momentum. The hope is that this progress will be sustained and see us to the end of the recession.

Two timeframes are available in Chart 2: December 2007 to present or a closer look at just 2020 and 2021. Total employment is available for both timeframes and specific industries are available for the more recent period.

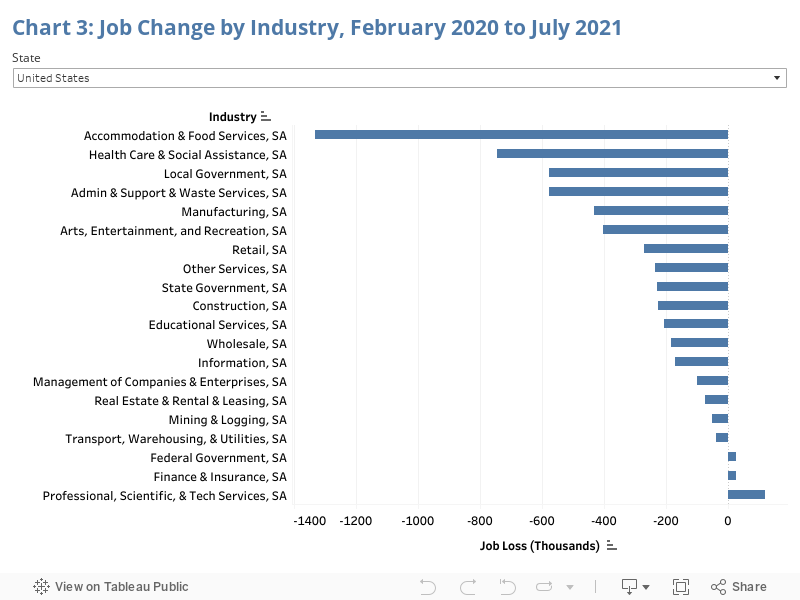

Chart 3 shows the change in employment for the selected state or area for each industry (or for some states, sector). Accommodation and Food Services has contributed the most to job loss in every state that is still down jobs except Iowa, where Health Care and Social Assistance is hit the hardest; Montana and Oklahoma where Local Government is the largest source of seasonally adjusted job loss; and North Dakota and Wyoming, where Mining and Logging has contributed the most job loss. Although job loss in Accommodation and Food Service top the list in most states, the extent of job loss in that industry varies substantially. Net job loss since February 2020 in the hotels and restaurants that comprise this industry range from highs of 41% fewer jobs in Washington, DC and 27.2% fewer jobs in New York to a jobs gain in Idaho of 1.7% and losses of less than 2% in Montana and Oklahoma and 6% in Texas—through July.

- “SA” indicates that the data for the sector or industry are seasonally adjusted. “NSA” indicates that the data are not seasonally adjusted.

Beyond Accommodation and Food Service, Health Care and Social Assistance, and Administrative and Support and Waste Management Services are still down significantly in payroll employment in most states. Within Health Care and Social Assistance, industry losses nationally have been mostly in Nursing and Residential Care Facilities and Social Assistance. Social Assistance includes Child Day Care, which is down 11% nationally in employment as of July. Selecting the bars in the charts will show the change in employment for that industry or sector from February 2020 to July 2021 as well as this June to July.

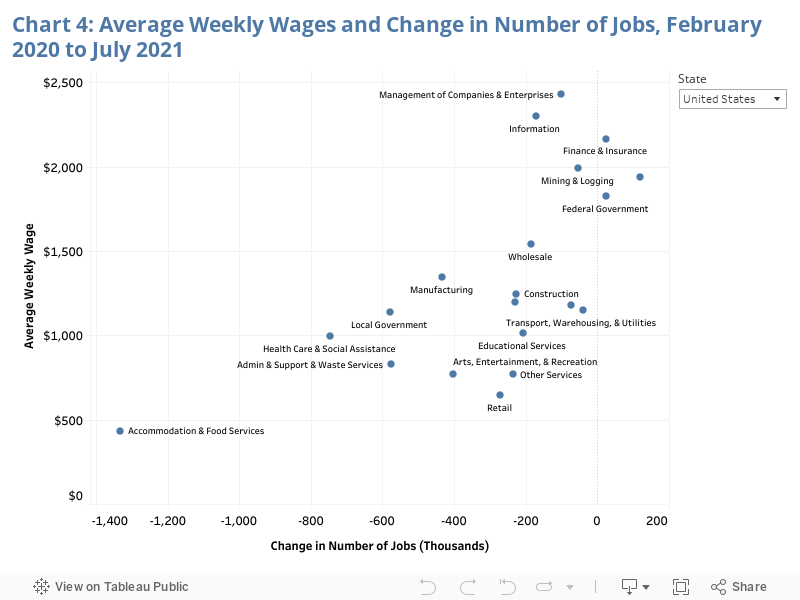

Chart 4 shows the relationship between job loss and average weekly wages for each industry. The overwhelming number of jobs lost have been in low-paying industries. Nationally, Accommodation and Food Service was down 1.3 million jobs as of July and had an average weekly pay of $433 in 2019. Health Care and Social Assistance was down 747,000 jobs in this time period, and Administrative and Support and Waste Management Services was down 577,000 jobs. These industries’ average weekly pay nationally were $996 and $828 respectively. Meanwhile, Management of Companies and Enterprises had lost fewer than 100,000 jobs, Finance and Insurance gained over 25,000 jobs, and Professional, Scientific and Technical Services gained 120,000—industries with average weekly pay of $2,429, $2,166 and $1,937 respectively.

- Hourly pay levels are not available as comprehensively as weekly wages at the state level so they are not used here, but the pattern for hourly wages is similar to the pattern for weekly wages.

These wage levels are, of course, averages across a wide range of jobs within the industries. Finance and Insurance includes both the heads of Wall Street firms and bank tellers. It is clear, however, that job loss has been significantly more acute in low-wage jobs than high-wage jobs. Low-wage employees are obviously much more heavily impacted by job loss. They have less in savings, and those who had employer-provided health insurance are less likely to be able to afford continuing coverage.

Table 1 shows the percentages of job loss for each industry in the country, selected state, district, or territory. Industries with more employees are, of course, more likely to contribute more greatly to the total numbers of job losses shown in Charts 3 and 4—just as larger states contribute the most to national job loss. From the perspective of an employee, customer, owner, or other stakeholder in an industry, the level of impact is measured best by the percent of jobs in the industry that have been lost. It is notable that, when looked at this way, Accommodations and Food Services and other low-wage industries are extremely hard hit. Thus, the reason that large numbers of low-wage workers in these industries have lost their job isn’t just that there are large numbers of them in these industries—it’s also that the industries have been particularly impacted by the pandemic and ensuing recession. Significant higher paying industries have not lost as large of a share of their jobs. The result is that not only are a large number of waiters out of work, but that a waiter is much more likely to have lost his or her job than a banker.

- “SA” indicates that the data for the sector or industry are seasonally adjusted. “NSA” indicates that the data are not seasonally adjusted.

Map 2 shows the unemployment rate. This measure is less reliable than usual under current circumstances. It is a measure of those who are not employed as a share of those who are employed or seeking employment. How respondents respond to survey questions related to whether they are seeking employment in this unusual period is not consistent, which makes the unemployment rate less informative. Also, people are not returning to the labor force—making themselves available for work—at a consistent pace across states. Some states are ahead, some behind, each month. Differences between states in unemployment rates are as likely to reflect timing differences month-to-month in people starting to seek employment as actual job creation. In fact, at times, strong job creation can actually elevate the unemployment rate: as jobs become more plentiful more people believe they have a prospect to get a job and enter the labor force, which raises the unemployment rate.

- Employment data are seasonally adjusted.

The problematic nature of using the unemployment rate as a measure in this volatile time as people re-enter the labor force is accentuated by the fact that many states have unemployment rates that have not been considered highly elevated in the past, yet they are still down substantial numbers of jobs. There are other measures of unemployment that address the problems in part, but they are not available by state on a monthly basis.

The highest unemployment rates in July were 7.7% in Nevada and 7.6% in New Mexico, New York, and California. Nebraska had the lowest unemployment rate at 2.3%. The United States as a whole had an unemployment rate of 5.4% as of July 2021. Clicking on a state in the map will show the rates for February 2020 (pre-pandemic), April 2020 (the worst month of the Covid Recession), and the four most recent months. The chart in Addendum 2 plots the unemployment rate from 2008 through May for the country or selected state, district, or territory.

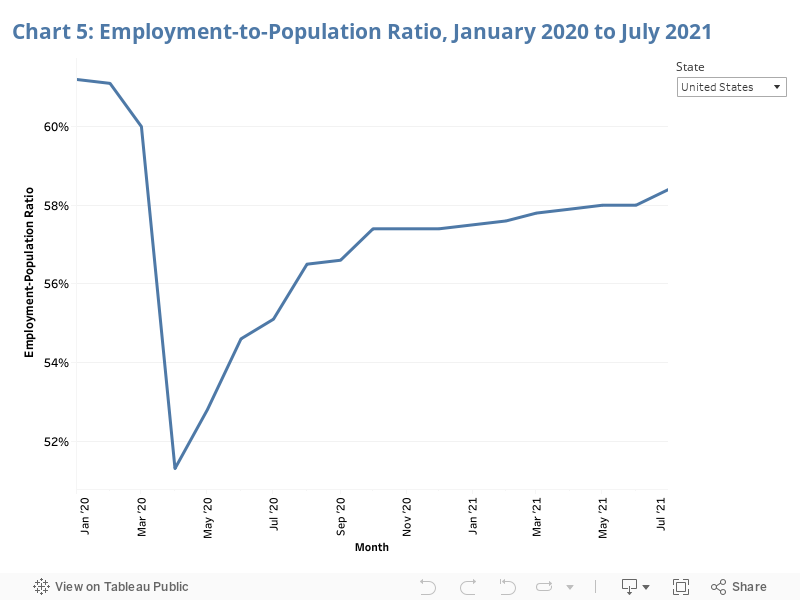

Employment-to-Population Ratio

Chart 5 shows the Employment-to-Population Ratio (EPOP) for 2020 and 2021. This is the percent of the population that is gainfully employed. For the country and most states, it has dropped significantly since February 2020, with only a slow recovery since then that stalled in October and has increased slowly through the first seven months of 2021. In the short term for any individual state, EPOP is a useful metric for gauging the share of the population who is employed, since unlike the unemployment rate it considers the entire population, not just those in the labor force. In the long run this measure is influenced by factors such as the aging of the population out of prime working years. The dramatic economic impact of COVID-19, however, currently dominates this measure.

- Employment data are seasonally adjusted.

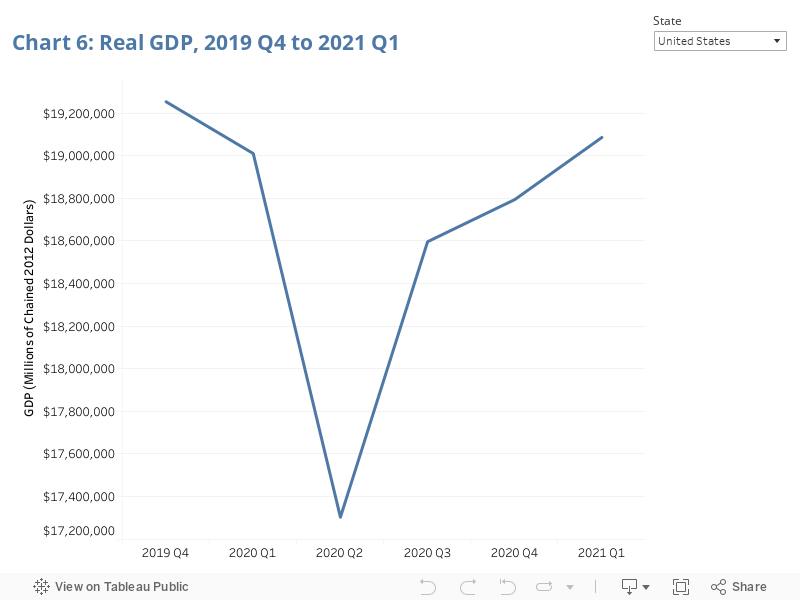

Overall Economic Activity

Economic activity, as measured by Gross Domestic Product, was down significantly in 2020. Through the first quarter of 2021, however, 14 states have seen increased GDP relative to their pre-pandemic baseline. The other 35 states and the District of Columbia still have smaller economies than they did prior to the pandemic recession. Map 3 shows the change in GDP by state between the final quarter of 2019 (just before the pandemic began) and the end of the first quarter of 2021. The size of the economy shrunk in every state during 2020, but through the first quarter of 2021 GDP change in states was more variable. The largest GDP increase over this time period was 4% for Utah. At the other end of the spectrum, GDP loss was still over 5% in Hawaii and Wyoming.

1. Real GDP, Chained 2012 dollars. GDP data are from the Bureau of Economic Analysis.

Chart 6 shows Gross Domestic Product from the end of 2019 through the first quarter of 2021. Each state and the United States can be selected. Nationally, GDP remained 0.9% lower at the end of the first quarter of 2021 than it was at the end of 2019 following a small drop in the first quarter of 2020 and a cataclysmic drop in the second quarter of the year. The second half of 2020 saw a significant GDP rebound in Q3, with smaller national GDP increases in the final quarter of 2020 and first quarter of 2021. It is estimated that the national economy has recovered all its lost ground as of the second quarter of 2021, but is still below what it would have been had the economy enjoyed even modest growth.

A sortable table in Addendum 3 provides both the total GDP change during the COVID-19 pandemic recession as well as the GDP loss during the Great Recession for each state. It is notable that although job loss had remained worse than in the Great Recession through the first quarter of this year, that was not true nationally for GDP. This reflects the particular impact of the current recession on labor-intensive service industries. Despite the improvement nationally, GDP loss during the pandemic recession remains worse than during the Great Recession in 8 states.

1. Real GDP, Chained 2012 dollars. GDP data are from the Bureau of Economic Analysis.

View Addendum 1: Sortable Jobs Table

The table in Addendum 1 can be sorted by percent change in employment, change in the number of jobs, or alphabetically by state. Different sectors and industry can be selected.

View Addendum 2: Unemployment Rate 2007 to present

Addendum 2 shows the unemployment rate by month from January 2007 to the most current month for which data are available. The national total or individual state, district, or territory can be selected.

View Addendum 3: Sortable GDP Table (2019 Q4 - 2021 Q1)

Addendum 3 shows GDP change from pre-pandemic through the first quarter of 2021 for each state.