{kind=link}

Monthly updates to the COVID-19 Economic Crisis: By State report has ended as of Oct. 2021. You can find the latest research published by the Carsey School of Public Policy on our Publications webpage.

Key Findings

The country as a whole has recovered nearly 80% of the jobs lost between February and April of last year. Some states have returned to pre-pandemic levels of payroll employment while a few states have regained fewer than half the jobs they lost.

The number of states with employment more than 5% below pre-pandemic levels is down to 18.

Many of the states that still face the largest jobs shortfalls are seeing relatively strong job growth in 2021.

Every state is on the economic mend from 2020’s pandemic-induced collapse in employment, when the country lost over 22 million jobs between February and April. As of the September 2021 Bureau of Labor Statistics (BLS) monthly survey of payroll employment, the nation overall has recovered close to 80% of those jobs. Individual states have ranged from recovering 36% of their lost jobs to recovering all of them. Many of the lagging states, however, have been catching up in 2021. Gross Domestic Product (GDP) has followed a similar pattern as jobs.

The collapse and the recovery have not been consistent across industries. Many industries in many states have fully recovered, while others have not. The Leisure and Hospitality sector, including restaurants, hotels, and entertainment venues, continues to be the largest contributor to the overall jobs shortfall.

The economic consequences of COVID-19 have been significant for the country and every state. The number of jobs lost and the decline in economic output were catastrophic, and many people were hurt financially, in many cases severely. The level of human deprivation was much less than it would have been, however, because of substantial intervention by the federal government.

Progress from the Low Point

Job losses nationally were at their worst in April of 2020 when the nation and every state had lost more jobs between February and April than had been lost in the Great Recession a decade before. Overall the economy has recovered 78% of those jobs, though that number obscures substantial variation by state. As shown in Map 1 and in the sortable table in Addendum 1, two states—Idaho and Utah—have recovered all their jobs and surpassed their total pre-pandemic employment. Arizona has recovered 94% of its lost jobs and Montana 90%. Others have fared less well. Wyoming has recovered only 36%, Louisiana 38%, and Hawaii 43%.

- Employment data underlying this map are seasonally adjusted, meaning that the Bureau of Labor Statistics accounts for normal seasonal variation in employment due to various factors.

- Small differences between states may not be statistically significant.

The Labor Market Now

Map 1 is a good comparison of how far states have recovered in employment relative to their low points at the depths of the pandemic recession. It does not, however, offer a good comparison of the current strength of their labor market because some states are recovering from worse downturns than others. If two states have both recovered half of their lost jobs but one lost 20% of its jobs from February to April 2020 and one lost 10 percent, the state that initially lost 20% is still down 10% of its jobs while the state that lost 10 % is now down 5 percent of its jobs. Even though they’ve both recovered the same share of lost jobs, the state that was hit harder initially has a substantially worse labor market than the state that was hurt less to begin with.

Map 2 and the sortable table in Addendum 2 compare current employment levels to pre-pandemic employment levels: the percent change in jobs from February 2020 to September 2021. Utah and Idaho have seen job increases over this period, with gains of 3.0% and 1.5% respectively. At the other end of the spectrum are states which (despite recent strong job growth in some cases) are still significantly short of their pre-pandemic employment: Hawaii, New York, Louisiana, and Alaska are down 13.0%, 8.9%, 8.8%, and 7.4% respectively. For comparison, jobs nationwide are 3.3% below their February 2020 level.

The patterns seen in Map 2 are not, of course, solely due to the recession and recovery. Each state had pre-existing employment trends. To fully assess the impact of the recession and recovery those trends have to be accounted for. After all, Texas, which ranked 8th in job growth in 2019, is not just missing the jobs it lost from February to April of 2020 but also the jobs that would have been otherwise gained.

The employment picture changes somewhat when looked at in the context of state trajectories prior to 2020. Map 3 shows states’ job shortfalls relative to what their employment levels would have been if their 2019 employment trends had continued. Looked at this way, all states are below their trend. Utah is, however, only about one percent below trend. Mississippi, Nebraska and South Dakota, which had been experiencing slow job growth prior to the recession, are only about 2% below their pre-COVID trend, as is West Virginia which had experienced job decline. Even as Hawaii, Nevada, and New York have seen improved job gains in 2021, they are still deeply affected by what happened in 2020—with Hawaii falling 12.9% short of its trend employment, Nevada 10.5% and New York 9.8%.

- Employment data underlying this map are seasonally adjusted, meaning that the Bureau of Labor Statistics accounts for normal seasonal variation in employment due to various factors.

- Small differences between states may not be statistically significant.

- Authors' calculations are based on seasonally adjusted data.

The Path of Recovery

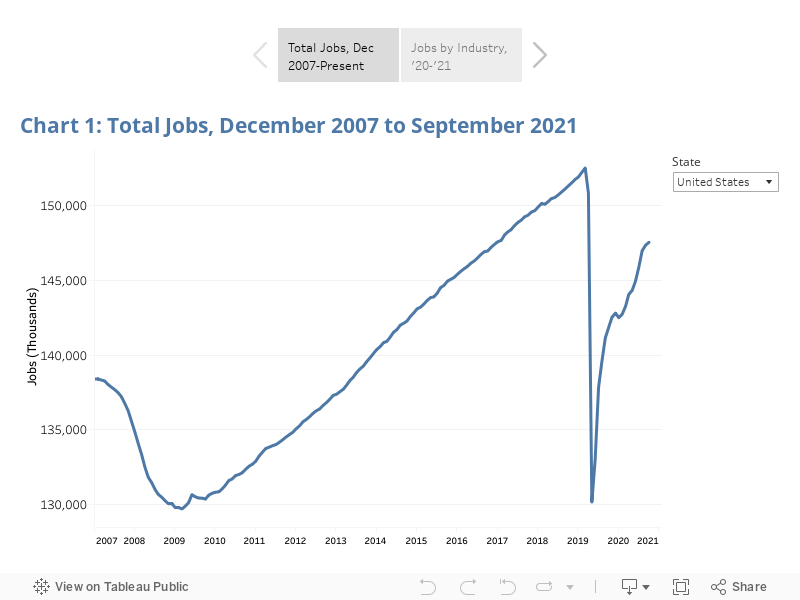

Chart 1 shows in stark fashion the extent of job loss at the beginning of the pandemic, the immediate partial bounce back, the slowing of the recovery later in 2020, and the pickup in February 2021. Prior to 2020 there had been a steady climb nationally out of the Great Recession that took hold in 2010, accelerated starting in 2012, and had slackened in the last few years. Then, between February and April 2020, in the country and almost every state, all or most of the jobs gained since the Great Recession were lost. Selecting the close-up view of 2020 and 2021 in Chart 1 reveals that the sharp drops of March and April of 2020 reversed in May, but the rate of progress slowed and even reversed in some states at the end of the year and into January 2021. Starting in February of this year, growth again accelerated. The latest month, September, however, saw a slowing of progress.

- Employment data are seasonally adjusted.

The path of the economy since February 2020 has been influenced by the prevalence of COVID-19 and the federal government’s response. The first flood of cases in early 2020 caused massive job losses. The economy began to bounce back as governments responded, cases declined, and businesses and people adjusted. In the latter half of 2020 and into January 2021, however, cases again rose and federal government support tailed off, leading to a slowing of economic progress. As strong steps by the federal government started to have an impact in February and March and optimism about the health situation grew, the economy regained positive momentum. In September, however, COVID accelerated and the economic recovery de-accelerated. The hope is that with cases again falling off this progress will renew and see us to the end of the recession.

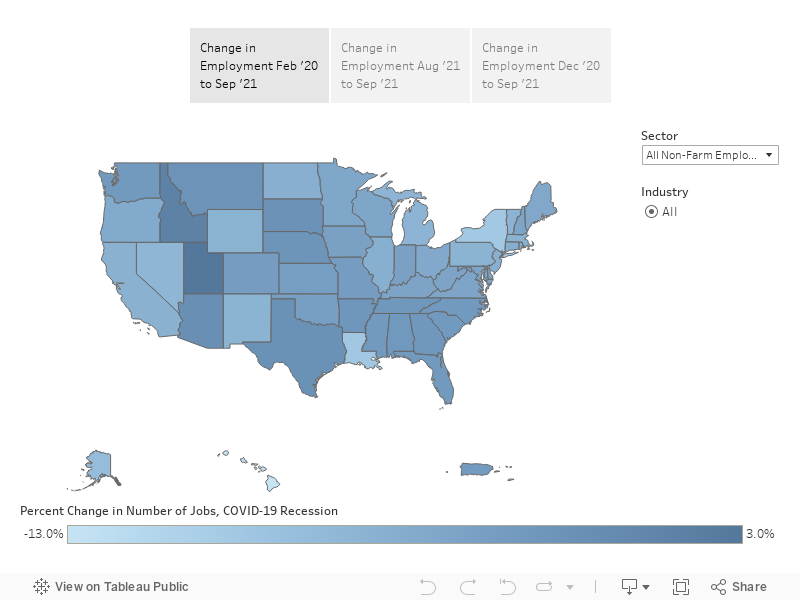

Chart 1 shows that the pace of recovery has changed a great deal over time, but these changes have not been consistent among states. Map 4 and the sortable table in Addendum 2 show that so far in 2021 Hawaii, Minnesota, Nevada, Washington, Rhode Island, Massachusetts and Oregon have seen the strongest job growth relative to their February 2020 employment levels. The slowest growing states by this measure have been Louisiana, Wyoming, Alaska, Arkansas, and Mississippi.

A comparison of Map 4 to Map 2, or looking at the table in Addendum 2, shows that many of the states that have the farthest go to reach pre-pandemic levels of employment have grown relatively faster in 2021 and vice versa (hovering over states on Map 4 reveals job growth in 2021 and the current jobs shortfall—which for comparison is 3.3% nationally). More detail on job growth in 2021 can be found in the sortable table in Addendum 3.

- Data are seasonally adjusted.

- Small differences between states may not be statistically significant.

For example Hawaii, which has the largest payroll employment shortfall, is first in job growth so far this year—recovering by 5.2% of its February 2020 level. Nevada, Massachusetts, and California are other states with high shortfalls that are doing particularly well this year. Conversely, some states that have done less poorly overall, Idaho, South Dakota, Montana and Arkansas, for example, are growing more slowly than many other states at this point. This suggests that the “last mile” to recovery may be more difficult. While surviving businesses can return to prior employment levels there are businesses that were lost in the recession and recovering those jobs may take longer as new businesses replace them or other businesses expand. In addition, some changes to the economy may be permanent, which will reduce staffing requirements in some industries. Other jobs will presumably replace the ones lost, but the shift will take time. There are many unknowns in how the economy will recover from this unique recession.

The pace of recovery is likely to continue to vary among states. Thus far, a number of factors have affected how states have grown relative to each other. As COVID-19 cases have ebbed and flowed, so have state economies. States’ reliance on different industries have also caused differences among states—with the states most reliant on tourism particularly struggling. States that were hit harder earlier have had a harder time coming back. These and other factors have, and are likely to continue to, cause the path back to be uneven geographically at particular points in time.

Industries

The recession hit different industries differently and they have recovered at different paces. Industries can be selected in the 2020-2021 view in Chart 1 to see how, nationally and in each state, they were affected and have recovered.

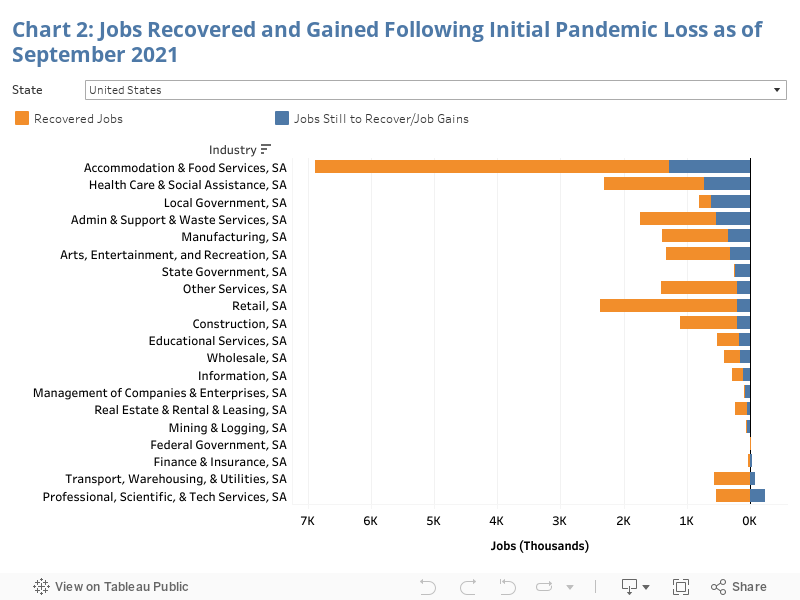

In Chart 2 the total length of the line to the left of the axis represents the total jobs lost from February to April in 2020 in the industry. The orange part of the bar represents the number of jobs that have been recovered of those that were lost. The blue shows the number yet to be recovered or, if to the right of the axis, the number above the February 2020 level. Selecting the bars shows the jobs lost from February to April, the number of those jobs recovered, the remaining shortfall or surplus, the total number of jobs gained since April 2020, and the job change in the last month.

- Employment data used here are seasonally adjusted, meaning that the Bureau of Labor Statistics accounts for normal seasonal variation in employment due to various factors.

- Initial pandemic loss covers period between February and April 2020.

- Employment data used here are seasonally adjusted, meaning that the Bureau of Labor Statistics accounts for normal seasonal variation in employment due to various factors.

- Initial pandemic loss covers period between February and April 2020.

The hardest hit sector from the beginning of the pandemic has been Leisure and Hospitality. Within that sector nationally, the Accommodation and Food Services industry has recovered 81% of its jobs and the Arts, Entertainment and Recreation industry 76%. Despite those recoveries, Accommodation and Food Services still shows the largest industry shortfall. It is down 1.3 million jobs, 8.9% off its February 2020 level. New York is still down 26% of its jobs in this category, the worst in the nation, with Hawaii, Nevada, Alaska and Massachusetts also with job shortfalls of over 20%. Jobs in this industry are up in Idaho by 2.9% and there are shortfalls of less than 5% in Oklahoma, Utah and Montana. The Arts, Entertainment, and Recreation industry is still down 316,000 jobs nationwide, 13% below pre-COVID levels.

State and local government employment also saw a dramatic initial drop. Nationally, state governments have collectively continued to lose jobs even during the recovery, while local governments have only added back 23% of the jobs that were lost earlier. Combined, state and local governments are still down 874,000 jobs from February 2020—over 4% off of pre-COVID levels. Wyoming has 12.1% fewer state employees, the largest shortfall in the country, with North Carolina next at 11.4%, followed by Mississippi at 10%. Local government employment is down the most in New Mexico at 11.2%, followed by Vermont at 8.3%, Connecticut at 7.8%, and Arkansas at 7.3%. Only 5 states have restored their state governments to pre-COVID employment levels and in only 3 states have the jobs in local governments been restored. Nationally, cuts in education employment are a disproportionately large share of the state government shortfall (75%) and about proportional to their share of local employment (50%).

The Health Care and Social Assistance sector is responsible for a large portion of the employment shortfalls in most states and while 69% of the jobs lost nationally have come back, payroll employment is still down 728,000 jobs. Three states have fully recovered their lost jobs. Although there are a very large number of jobs still to be recovered in this industry, that has as much to do with the large size of the sector’s workforce as with how severely it was impacted by the recession. In percentage terms this sector is less hard hit than the hardest-hit industries, down by about the average for all industries combined. The shortfalls in the sub-categories of this sector have varied greatly and, as of September 2021, are mostly in Nursing and Residential Care Facilities and Social Assistance. Social Assistance includes Child Day Care, which is down 10% nationally in employment.

Two private sector industries—Professional, Scientific and Technical Services, and Finance and Insurance—have returned to their pre-COVID level of employment nationally. They have fully recovered in 36 and 20 states, respectively. Other industries have recovered to pre-COVID levels of employment in many states—Construction has returned to pre-recession levels in 14 states, Manufacturing in 8, and Retail Trade has recovered in 17 states, for example.

Table 1 shows the percentages of job loss for each industry in the country, selected state, district, or territory. Industries with more employees are, of course, more likely to contribute more greatly to the total jobs shortfall shown in Chart 2—just as larger states contribute the most to the national jobs shortfall. From the perspective of an employee, customer, owner, or other stakeholder in an industry, the level of impact is measured best by the percent of jobs the industry is down from pre-pandemic levels. Although the level of employment in Health Care and Social Assistance is significantly down, sector-wide, it hasn’t been the sector where individuals have been the least likely to be able to retain or find employment.

That said, the Leisure and Hospitality industries head this list as they do in the quantity of missing jobs. Administrative Services are also still down significantly in percentage terms with Temporary Help Services being the largest area of jobs shortfall.

- “SA” indicates that the data for the sector or industry are seasonally adjusted. “NSA” indicates that the data are not seasonally adjusted.

Map 5 allows comparison of job shortfalls or gains by sector and industry. Three views are available: (1) from before the recession began in February 2020, for 2021, and for the last month. Selecting states on the map shows the change in employment in total jobs and percent change relative to pre-pandemic employment by selected time period, sector, and industry. Additional detail can be found in the Addenda.

Map 5: Change in Employment, June 2021 to September 2021

- Employment data used here are seasonally adjusted, meaning that the Bureau of Labor Statistics accounts for normal seasonal variation in employment due to various factors.

- Small differences between states in the percent job change may not be statistically significant.

- Employment data used here are seasonally adjusted, meaning that the Bureau of Labor Statistics accounts for normal seasonal variation in employment due to various factors.

- Small differences between states in the percent job change may not be statistically significant.

Employment-to-Population Ratio

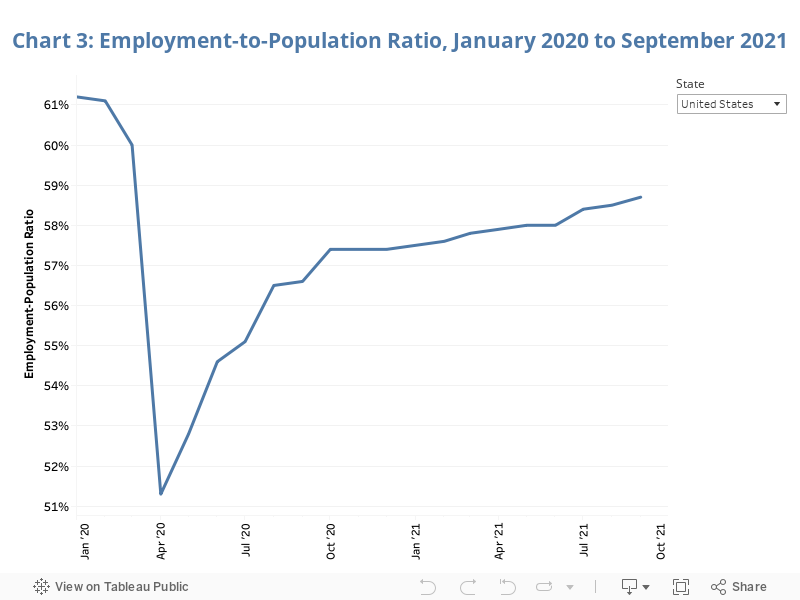

Chart 3 shows the Employment-to-Population Ratio (EPOP) for 2020 and 2021. This is the percent of the population age 16 and over that is gainfully employed. It dropped precipitously as jobs were lost at the beginning of the recession and rebounded through the summer of 2020, but has been coming back only slowly (although fairly steadily) since then. In the short term, for any individual state, EPOP is a useful metric for gauging the condition of its labor market. Its advantages over the employment data referenced above are that it includes all employment, including the self-employed, and adjusts for population—one would expect job gains as population grows under any circumstance. It is, however, based on a relatively small survey sample at the state level and provides less detail than payroll employment data.

It is also not useful for comparing state labor markets with each other because other factors, such as the age profile of the population, have a significant impact on the measure. Also, while useful in the short term, over time this measure will make the recovery look less robust than it is as the overall aging of the population results in a lower percentage employed due to retirement.

In September 2021, Nevada and California had the highest unemployment rates in the country, both at 7.5%. Nebraska (2.0%) and Utah (2.4%) had the lowest, while the national unemployment rate was 4.8%. The unemployment rate is a widely used measure of labor market health, but the way it is calculated has given the metric mixed usefulness during this period. Unemployment is calculated by dividing the number of people currently not working but available for and actively seeking work, by the number of people in the labor force. It is the question of how many people are available for and actively seeking employment that has been challenging to measure. Many people who have wanted to work have not actually sought employment, constrained by health fears, child care challenges, and other impediments to seeking work. Not counting these would-be workers can make a state’s unemployment rate low even though the recovery, in the sense of jobs being created or restored, isn’t going all that well. In addition, large numbers of workers have left the labor force via early retirement and other decisions—which lowers the unemployment rate but is hardly a sign of a strong labor market.

- Employment data are seasonally adjusted.

The difference between states in the prevalence of these several factors is difficult to know accurately. Also, unemployment rates are affected by which industries are more dominant in the states—agricultural states tend to have low unemployment rates, for example. The weakness of this measure is highlighted by the fact that unemployment is almost down to its pre-COVID levels in some states despite a substantial jobs shortfall. Nevertheless, the unemployment rates reflected in Map 6 generally follow the pattern the payroll employment data presented above.

A graph showing longer term trends in the unemployment rate can be found in Addendum 4.

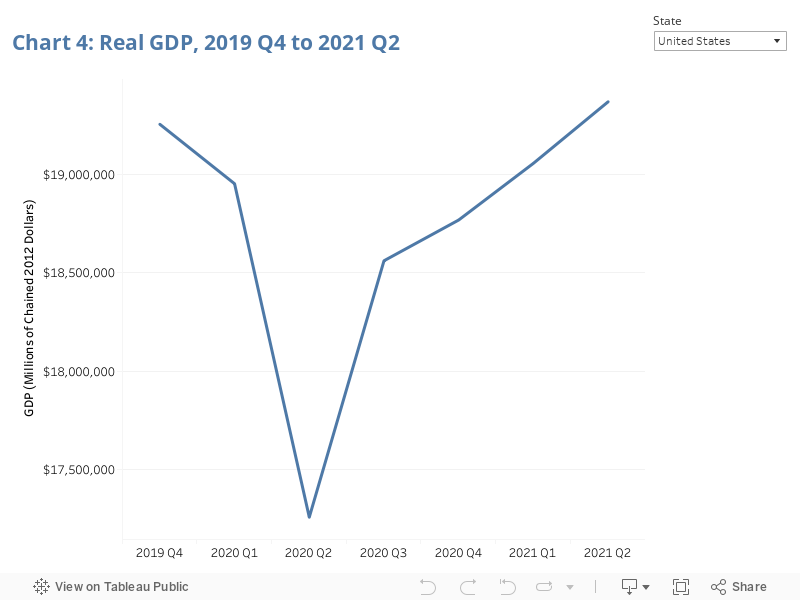

Overall Economic Activity

Chart 4 shows Gross Domestic Product (GDP) from the end of 2019 through the second quarter of 2021. Each state, the District of Columbia, and the United States can be selected. Nationally, GDP was 0.9% higher at the end of the second quarter of 2021 than it was at the end of 2019, making it the first quarter since the pandemic recession began where GDP was above pre-COVID levels. Despite the increased national GDP, it is still below what it would have been had the economy enjoyed even modest growth without the pandemic. Thirty states had a 2021 Q2 GDP that was higher than their 2019 Q4 GDP, while 20 states and the District of Columbia had a total economic output for the quarter that was still below pre-recession levels.

1. Real GDP, Chained 2012 dollars. GDP data are from the Bureau of Economic Analysis.

View Addendum 1: COVID Employment Collapse and Rebound Table

Addendum 1 shows the change in jobs from the low point of the COVID recession to the present. It can be sorted by percent change in employment, change in the number of jobs, or alphabetically by state. Different sectors and industry can be selected.

View Addendum 2: Where We Stand in Recovery 2021 Table

Addendum 2 shows the change in jobs from pre-pandemic to the present. It can be sorted by percent change in employment, change in the number of jobs, or alphabetically by state. Different sectors and industry can be selected.

View Addendum 3: 2021 Job Trends

Addendum 3 shows the most recent month's change in jobs. It can be sorted by percent change in employment, change in the number of jobs, or alphabetically by state. Different sectors and industry can be selected.

View Addendum 4: Unemployment Rate 2007 to Present Graph

Addendum 4 shows the unemployment rate by month from January 2007 to the most current month for which data are available. The national total or individual state, district, or territory can be selected.